What’s the deal with SPACs!

- March 31, 2021

- Posted by: Vishwas Sinha

- Categories: Finance & accounting, Transaction Advisory

Though Special Purpose Acquisition Companies (“SPACs”) have been around for a long time, 2020 has been a marquee year for them. A record number of companies have gone public through this method. Momentum is really in favor of SPACs, as opposed to IPOs, and this trend is poised to become a strong force this year. What is driving this change? Let’s take a deeper dive.

What is a SPAC?

As the name suggests, a Special Purpose Acquisition Company (SPAC) is set up solely for the purpose of acquiring an existing company. A SPAC is essentially a shell company with no commercial operations, set up by reputed investors to raise capital via an IPO to acquire an existing company. Since a SPAC has no existing operations – it makes no products, does not sell anything, and only assets it owns are the money invested by the founders and raised by the IPO – it is also known as a “Blank Cheque Company”. It essentially means that initial investors are going by the reputation of SPAC founders and putting faith in their value judgement. However, SPAC founders are some of the most well known investors with impeccable reputations and proven track records of successful investments.

How does a SPAC Work?

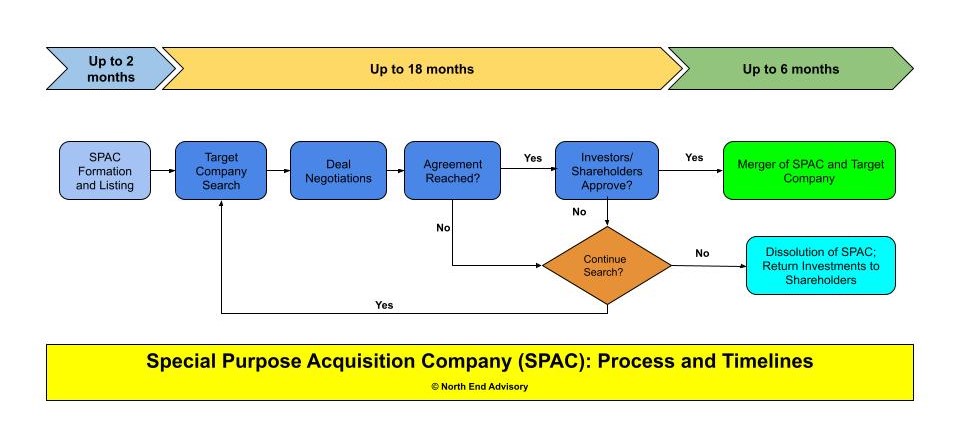

Founders satisfy the minimum capital requirements. SPAC board and management are constituted then who ensure proper setup and governance. Founders have the sole right to elect SPAC directors. Once the SPAC is formed and registered with the SEC (or the applicable governing body in that territory), it raises more capital via an IPO (founders’ shares: public shares ratio is typically 20:80). The SPAC’s IPO is typically based on an investment thesis focused on a sector and/or geography, such as the intent to acquire a FinTech company in North America, or based upon the founders’ experience and background. This capital is put in a Trust for a set period of time (2 to 3 years generally). The public shareholders receive “Units” offered via that IPO; each unit consists of a common share and a fraction (1/2, 1/3rd or 1/4th typically) of the warrant. Founder shares and public shares generally have equivalent voting rights; but warrants don’t. Only whole warrants are exercisable.

Once the capital is raised with the sole intention to acquire a company, the search for a target company starts. Once a target company (that meets the investment criteria) is identified, negotiations take place. If an agreement is reached, the intent to merge is announced with the Capital already earmarked for the purpose and sitting in the Trust. The SPAC’s public shareholders may choose to vote against the transaction and elect to redeem their shares (this protects them against scams or poorly made acquisitions). If the SPAC requires additional funds to complete a merger, the SPAC may issue debt or issue additional shares, such as a private investment in public equity (PIPE) deal.

If the merger is approved, the target company is acquired and then quickly integrated into the SPAC (also known as “De-SPAC”). In case the negotiations fell through, the search is continued. If no target company could be identified within the stipulated time frame (2 or 3 years), then capital is returned to the investors with accrued interests at market interest rates.

Why SPACs are all the rage?

Current SPACs set ups offer very generous incentive structures to the SPAC founders. Since they typically receive 20% equity convertible to common shares, they have lots to gain from a successful acquisition. Even if the acquired company doesn’t have a strong business at the time of acquisition, companies with good growth potential and reputed investors would attract a lot of positive attention from retail investors. Besides, such companies would attract buyers of their products/services and talented employees.

SPACs offer a lot of value to individual investors as well. They have the upside to get in early on a very lucrative deal (with reputed investors and experienced managers) and their downside is very well protected – investors can get their money back if they choose not to approve an upcoming acquisition. Moreover, if the SPAC cannot find a desirable company to acquire, investors will still get a refund on their initial principal. In a nutshell, investors can make significant gains in a short timeline (average SPAC deal time is 6 months) and with low risks.

Other than SPAC founders and investors, target companies may also have a lot to gain. In the months preceding the COVID outbreak, several companies chose to postpone their IPO plans due to valuation uncertainties. Some IPO fiascos made the companies more cautious against going public via an IPO. Unlike IPOs, SPACs offer more clarity and visibility around target company valuation. This helps alleviate valuation uncertainties, especially in the time of pandemic and political changes where there are legitimate concerns about economic recovery and unemployment rates.

As you can see, SPACs are currently offering so much value to all participants. No wonder there have been a series of high profile SPAC transactions just over the last year.

What are the benefits of SPAC?

SPACs offer many benefits that shorten the deal timelines and increase the confidence of both investors and target companies. First of all, SPAC are set-up with the clear mandate of acquiring a company, so the mindset and willingness to acquire is there from the beginning. From that sound footing, SPACs go on to offer many benefits:

Finance and Investment: The fund for acquisition is already there with SPACs, so there isn’t much ambiguity or uncertainty about investor’s ability to finance the deal. Each SPAC is founded and governed by reputable persons. The funds stay in a Trust (or an escrow) until it’s used, so the downside risk is very little for the investor. In case a deal never materializes, the investors get their money back with the going interest rate; they only fail to earn the market’s return that would vary by how they invested their fund alternatively. The upside, on the other hand, can be significant.

Fixed Timelines: SPAC timelines are not open-ended that could linger into years. A SPAC is set with an expressed purpose (and funds) to acquire a company within a maximum of 2 years. If not, then SPACs have to get dissolved and return the money to the investors with the going interest rate (note – some jurisdictions allow an option to extend a SPAC for a maximum of 1 year, but that option is often not pursued). Besides, unlike PE or VC investments that have a longer lock-in time (average 5-10 years) for investments to come to fruition, SPAC can bring significant RoI over a much shorter time (average SPAC deal time 6 months).

Regulatory: SPACs allow fast closure of deals as they typically do not involve as many steps, filings, and approvals as an IPO. Investors in a SPAC are more aware of the purpose, so the risk is typically considered low. Target companies, on the other hand, get acquired by a newly minted company – so there are not many skeletons in the cupboard that regulators need to worry about.

SPACs are Typically Clean: As stated previously, since SPACs are newly minted companies and founders’ reputation is key to their success, SPACs are typically very clean. There is generally no rot to be found. Founders and underwriters history can be obtained by the investors and the target companies. If any taint is found out via their due diligence process, investors and target companies have every right to stay out of such SPACs.

Greater Say Available to Investors: Unlike PE or VC companies, where the Venture Partner or Fund Manager decide on the deal on their discretion, SPAC deals have to go through the scrutiny of the investors who get to vote on any opportunity presented. This by itself is a solid reason for many retail investors to prefer SPACs over other investments.

Seasoned Management: SPAC boards and management teams are usually filled with SMEs of their areas. The success of this management depends upon the success of their SPACs, more precisely the RoI for the founders and investors. For the same reason, they have both the founders and investors looking after their performance. Seasoned managers know all of this. That is why, even after a SPAC merger, it is a common practice to keep some of these experts in the management teams or in the board for an active role within the company.

How does a SPAC compare with the traditional IPO?

In addition to the values mentioned above, SPAC offers several other benefits that a traditional IPO doesn’t.

Less Time and Costs: For years, companies used reverse mergers as a faster and quicker workaround to IPOs. But a SPAC offers even greater advantages than a reverse merger. In a SPAC transaction, the money has already been raised, so negotiations with underwriters are often unnecessary. Besides, an IPO has to satisfy a lot more criteria than a SPAC. Since SPACs are considered less risky, the regulatory and compliance aspects of the deals are also less complex, which suits both the target companies and the investors. Needless to say, the associated costs of advisors, legal, tax, bankers, paperwork etc. are much less for a SPAC transaction. All this put together make SPACs a quicker and cheaper alternative to an IPO.

No IPO “window” required: a lot many IPOs have missed the mark because they missed the “right window”. Timing is everything for an IPO, not so much for a SPAC. SPAC market is almost always active. Success in a SPAC does not depend on a “pop”, but on the expert handling.

No Minimum Thresholds Required as in an IPO: Many smaller companies may not even qualify for an IPO because of the minimum threshold requirements. SPAC offers an alternative to such companies who won’t make that cut. Many such companies are actually good companies set up with innovative ideas and values, and have great growth potential. It is best that such companies get an opportunity out there.

Experience at Hand: SPACs typically come with an experienced team. This allows the target companies to work more efficiently on the deal than an IPO would.

No Capital Raising Event Required: There are no earth shattering capital raising events required for a SPAC. SPAC success does not depend on “first 4 hours” on the New Issue Day. There typically would be no one pushing the IPO through the markets over gullible investors. SPAC investors have all the tools to make a well informed decision without being pressured. Guess what, it is better for the companies as well! SPACs have the cash, they are already listed as a public company, and they are just looking for a good fit company to buy.

Right to Reject SPACs: Companies going public via an IPO have no control over how it pans out. It all depends upon market conditions and the buzz thus leading to “pop”. However, companies going public via a SPAC have all the right to reject offers if the terms are not acceptable to them.

Criticisms of SPACs

Despite all the benefits that SPACs have to offer, they have copped their fair share of criticisms. In our opinion, the top three criticisms of SPACs are:

Where is the money coming from: It might be difficult to find out who is financing the underwriters and founders. Most ethical people would not like to do anything with a company that’s been setup with shady money coming from authoritarian regimes, oligarchs, cartels, or other nefarious sources. That is why it is doubly important to ascertain founders’ reputation and do a thorough check on a SPAC.

Dilution of Shares: Founders of a SPAC often purchase large initial stakes as “founder shares” for a nominal amount at the time of formation. These shares auto-convert into common shares of the company post-merger (founder shares generally constitute 20% ownership of the total shares of the post-merger company). This could cause significant dilution of the company’s shares.

Some SPACs can be Outright Scams: As with anything trendy in capital markets, SPACs have attracted scammers looking to defraud investors. Even target companies would be setback by going in the hands of wrong investors. That is why we recommend both sides to utilize professionals to conduct thorough due diligence. Given the high stakes, SPAC should really be not done as some “Do IT Yourself” project.

How to Avail the Opportunities Presented by SPACs?

While SPACs present very good opportunities for both sides, it is important to do it well. Each step of the SPAC process is critical, and both sides can lose value very quickly. We highly recommend that both buyers and sellers in a SPAC transaction work with professionals and advisors who have strong work ethics and thorough knowhow of the process. A champion advisor would look into all aspects of SPACs and target companies, ensure mutual good fit, and recommend proper action items throughout the transaction lifecycle. Even after a merger is announced, professionals can help both buyers and sellers over numerous activities such as:

- Public Company Readiness

- SEC Reporting

- Market Communication

- Post-merger Integration & Governance

- Accounting

- IT Integration

- Project Management

- Financials

- Tax Structuring

- Audits

- Management Discussion & Analysis

- Form 8-K (“Super 8-K”)

- Synergy Realization and Value Creation

Conclusion

Despite prevailing concerns, the outlook for SPACs looks promising. Once the bubble starts to deflate, SPAC founders would find it harder to raise capital or good target companies to acquire. On the other hand, companies would find it harder to find good-fit SPACs. The landscape would become more competitive, with ROIs getting less generous for all stakeholders. There would invariably be SPAC Rockstars, also-rans, and failures; the landscape might become too difficult/expensive to navigate. But until then, SPACs would continue to offer significant advantages; smart founders, investors, and companies would take full advantage of this opportunity.